The First Home Super Saver Scheme (FHSSS) is touted as a way to make it easier for younger Australians to enter the property market by accessing their super.

However, only extra, voluntary contributions can be used for the property purchase.

This means that your savings for your deposit have to go into super, are taxed at lower than your marginal rates and then can be taken out.

In essence, it doesn’t release any of your employer’s compulsory super contributions made you’re your account.

The maximum you can contribute towards your deposit in super is $15,000 per year and a total of $30,000.

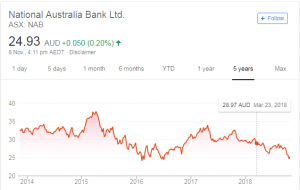

Given the small amount the scheme allows you to save relative to the amount of the typical deposit, the relative stability of the property market compared to shares (see graphs below for some examples of ‘blue chip’ share prices), the fact that wealth creation in Australia in many cases is dependent on home ownership and the way Australia’s age pension scheme favours home owners, it would make more sense to allow millennials to access some of their employer- contributed super to contribute to the deposit.